545MWp of new solar was installed in the UK last year, making 2020 the strongest year for solar deployment since 2017. Image: Lightsource BP.

The UK solar industry installed 545MWp (DC) of new solar PV capacity during 2020, the first full calendar year when no government subsidies were on offer.

This strong deployment level represents over 25% year-on-year growth compared to 2019 when FiTs were finally removed at the start of that year.

There are now three key segments for UK solar: residential, large commercial rooftop (typically 250kW and above), and utility-scale solar farms (capacity above 30-40MW). Each of these is expected to grow during 2021, pushing the UK into a key GW-plus subsidy-free market going forward.

This article talks through our in-house data supporting trends in deployment for solar in the UK, across the various rooftop and ground-mount segments of the market.

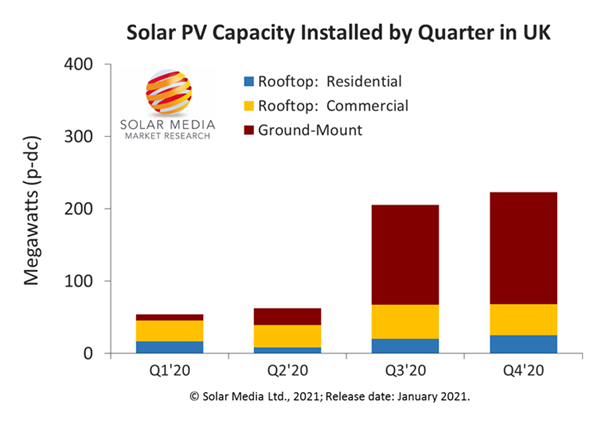

The first graph below shows the quarterly solar capacity deployed in the UK during 2020, split out by residential rooftop, commercial rooftop and ground-mount. The ground-mount part of the market is dominated by large utility-scale projects, which is important to differentiate from public-sector/utility-company small-scale sites.

The UK installed 545MW solar capacity in 2020, with a strong second-half, driven by a group of large-scale solar farms being built across England and Wales.

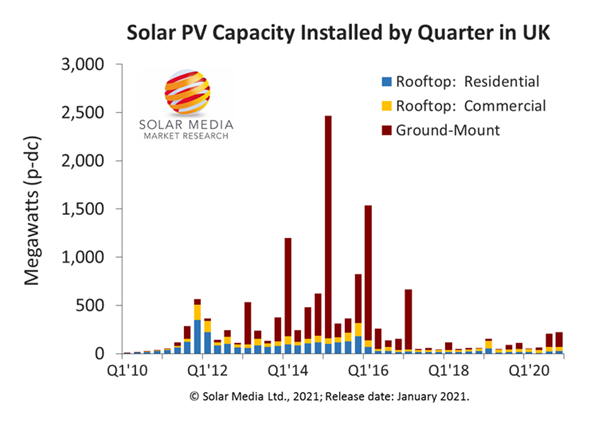

Putting this quarterly deployment into context, the graph below now shows quarterly deployment going back to the ‘start’ of UK solar in 2010. Clearly, the levels in 2020 are well below the massive peaks seen when the RO scheme was active in the UK.

Quarterly deployment of solar in the UK has traditionally been driven by step-down or discontinuation of government incentives through FiTs and ROCs.

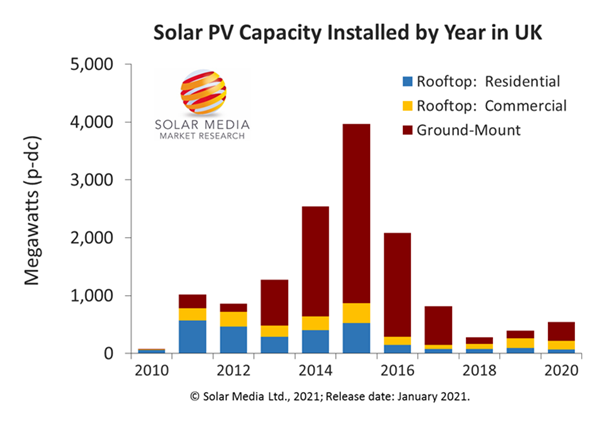

Instead of looking at quarterly lumpiness in deployment, it is more useful to look at calendar year figures. This is shown below.

The UK solar industry peaked in 2015, when almost 4GW was deployed. Further GW-levels occurred in 2017 and 2018 as ROs were finally exhausted. Since 2018, the industry has been in ‘recovery’ mode towards GW-plus in a subsidy-free environment.

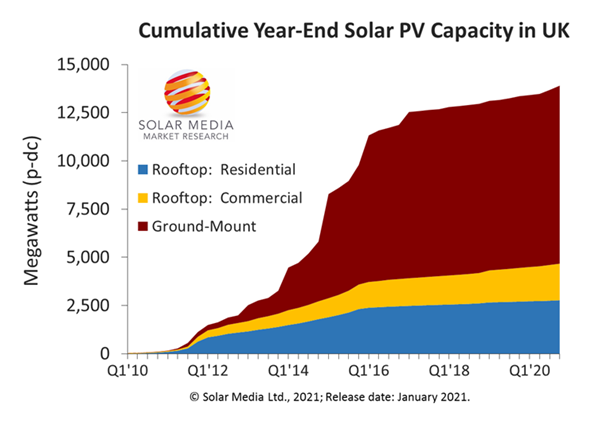

From a cumulative standpoint, there was 13.9GW of solar PV installed in the UK at the end of 2020. This is shown in the graph below. As expected from the figures above, overall deployment is dominated by ground-mounted systems (about two-thirds of capacity). About half of the ground-mount capacity comes from sites of 30MW and above.

Residential and large-scale ground-mount solar sites have dominated the UK solar landscape until now. However, the large commercial rooftop segment (specifically 250kW and above) is seeing its strongest quarterly deployment levels.

Over the next few months, we will be analysing quarterly deployment levels in more detail, across a series of features on Solar Power Portal. More information on this, or to access our in-house research databases for UK solar project activity, please complete details at the landing page here.