Image: RES.

The UK has a pipeline of 2.3GW of commercial and industrial (C&I) and utility scale battery-based energy storage projects, with many developers already looking to ‘stack’ revenues through providing multiple services, a new report has found.

Many of these developers are the same names that have been behind the rapid growth in utility-scale renewables that the country has seen over the past few years, including Anesco, Low Carbon and Green Hedge Energy, according to the UK Battery Storage Project Database, produced by the market research division of Solar Power Portal's publisher, Solar Media.

“Battery storage in the UK is poised to become one of the fastest growth segments within the country’s energy sector, often co-located with conventional or renewable generation,” analyst Lauren Cook said, adding that “the renewables sector has the most to gain from storage co-location, due to the variable supply from wind and solar”.

The UK’s energy storage sector has risen to international prominence over the past year due in part to the success of advanced energy storage projects in a tender to provide 200MW of enhanced frequency response (EFR) to the grid, as well as providing 500MW of a total 3.2GW of capacity procured in a recent capacity market auction, designed to ensure security of supply. More auction rounds are expected in various areas.

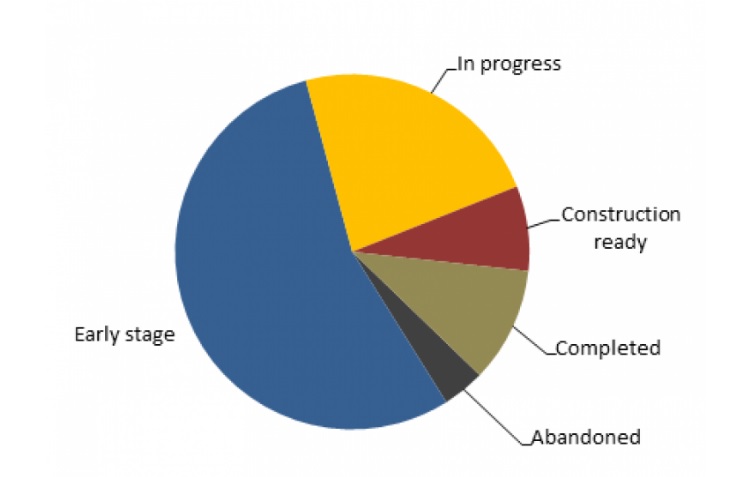

Cook’s team at Solar Media Market Research found nearly 200 energy storage projects at various stages of their development: some 90% are yet to be built while more than 50% are at an “early stage” of development, meaning the planning process is already underway and submissions to provide grid services have been made. The report was compiled through processes that included “data-mining planning portals, matching with projects submitted for grid connection approval or applications to provide grid services, and understanding the legal ownership of sites and the respective developers and planners,” Solar Media Market Research's head analyst Finlay Colville said.

Status of nearly 200 UK commercial & industrial battery storage projects, at January 2017. Image: Solar Media.

Revenue stacking and the dominance of Li-ion

“Lithium-ion does seem to be emerging as the dominant technology at the moment,” Lauren Cook told SPP.

“A lot of the planning applications don’t necessarily say the size of the project but they do say the technology, and what kind of ground space it’ll take up. So I think we might see some other technologies coming in on some of the pilot projects and some of the more innovative ones, but I think lithium-ion will be dominant this year.”

Cook also said the business models behind many of the projects in the 2.3GW pipeline appeared to show willingness from developers to provide multiple services in front of the meter, although she said the full picture is “still very much emerging”.

“We are seeing some developers starting to ‘stack’ revenues, as has been discussed a lot. They’ve got multiple contracts…you’ve got a lot of new businesses entering the market who will be able to manage those contracts for the asset owner, so I think that’s definitely something we’ll be seeing a lot more of this year.”

Based around the timing of frequency response and capacity market auctions earlier in the year Cook said there had been a “rush” of applications during the summer months, now slowing “to a trickle”. In future, while there would not be a subsidy-driven annual rush at the end of each financial year as had been seen in solar and wind, with no subsidies forthcoming for storage, many applications are likely to be structured around deadlines for future tender processes.

For more information and to purchase the UK Battery Storage Project Database click here.