Solar Media Market Research analyst Josh Cornes talks through the months since the government’s Clean Power 2030 Action Plan was published, addressing how grid connection queue reforms and the 2030 deadline have impacted the UK’s solar development pipeline.

With development status so crucial for grid connection queue position, developers are rushing to get planning applications in. A total of 30 applications went in during December alone, the second-highest month seen since March 2022, with only November 2023 outshining it.

These sites made up over 1.1GWp of capacity, a significant number seeing as they were all at Local Planning Authority (LPA) level. This late rush, alongside Botley West’s submission in November meant 2024 was the second-best year for applications in terms of capacity, only behind 2023.

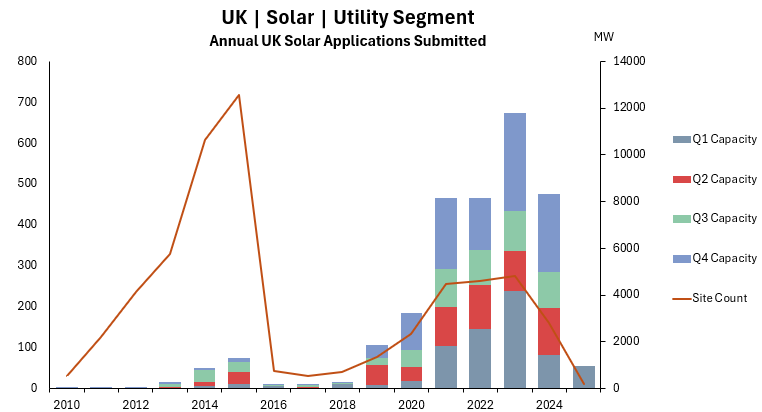

Figure 1 shows the two most active quarters for the three years prior to 2024, which were Q1 and Q4. However, Q1 2024 was noticeably quieter, while Q4 saw a large spike in capacity, the third highest we’ve seen.

The main reason for this influx of applications is due to the cutoff date of 20 December. Developers needed to submit an application before this date to show strategic alignment under the National Energy System Operator’s (NESO’s) Gate 2 methodology.

The applications from November 2024 – February 2025 came from over 35 different developers, with a number submitting their first applications. Looking into the projects themselves, some have had a grid connection for up to 6 years, with most having received offers pre-2023. This highlights the urgency Clean Power 2030 (CP30) has caused, causing developers to move on pre-existing projects, as some see the potential for their project connection date to be brought forward. One of the projects has a grid connection date as far out as 2036.

Awaiting planning approval

Developers are seeking planning approval on their sites before May, a crucial date for the upcoming grid reforms. Projects submitted in late 2024 will struggle to get approval by this date; there are currently 250 sites awaiting a decision, with over 150 being submitted before July 24 totalling 9GWp of capacity.

Figure 1 also outlines the size of projects currently going through development, with 2024 having a slightly higher capacity than 2021 and 2022, but 40% fewer projects being submitted.

There is also a large amount of movement on projects being submitted for scoping or going to local consultation. Q3 2024 alone saw 5.2GW across 55 projects start consultation or begin the process for a Nationally Significant Infrastructure Project (NSIP), with Q4 adding a further 2.5GW across a similar number of projects.

Similar to the influx of submissions in November/December, CP30 will be a large contributing factor to the jump. The average capacity in July-September being nearly 100MW per site means a significant amount of this capacity is made up of transmission projects, with projects such as High Grove Solar Farm, Mylen Leah, East Pye and the Droves all going into NSIP, with more starting local consultation.

There is an even larger spread of developers starting the early stage process of development. Since Q2 over 10 new developers have begun the process on their first sites in the UK. Some of these sites are companies moving on their existing grid connection for the previously mentioned reasons, and others are companies who are moving into the market, purchasing existing grid and land, taking the project through the development process and then building out.

Developers are moving fast on existing projects, either beginning the consultation process or submitting applications, with CP30 causing urgency in the market. Over 90% of the projects hitting the planning portals already have grid connection as developers attempt to jump up the queue, with some sitting on over 2.5GWp of distribution grid connection and 20GWp of transmission grid connection.

All the data above is taken from Solar Media Market Research’s analysis, which can be accessed here.

To book a demo and access the data please email [email protected].