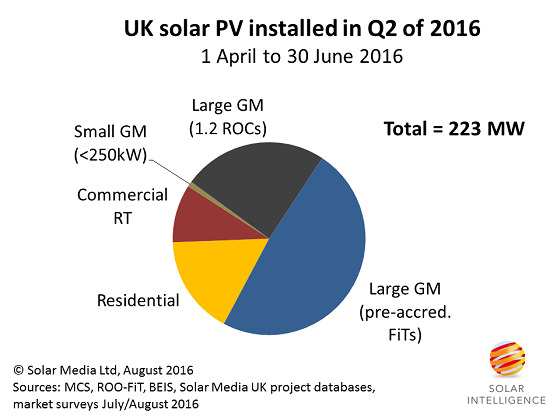

In-house market research conducted by Solar Media Ltd can now reveal exclusively that the UK added 223MW of new solar PV during the second quarter of 2016.

This comes after 1.55GW was installed during Q1 2016, bringing the H1 total to 1.78GW.

Deployment was once again heavily weighted to large-scale ground-mount, with over 70% coming from this category. This was a combination of 1.2 ROC and pre-accredited FiT sites all below 5MW, or on sites still forming multiple 5MW split locations.

Interestingly, residential is far from dead in the market, despite the FiT changes from January 2016. The quarterly rates now are about 25-40% of the levels seen during the period from mid-2012 to end-2015, when the rooftop segment was subject to quarterly degressions by government policy-makers.

The full split is shown below, with RT for rooftop and GM for ground-mount.

The UK installed 223MW during Q2’16, with large-scale ground-mounted sites contributing more than 70% of overall deployment in the quarter.

Within the dominant ground-mount segment, the majority is falling under pre-accredited FiTs (including community split-site builds). However, it is notable that the build-out of 1.2 ROC sites is relatively strong, a market that many industry players thought was going to be too high risk given all the (undefined) caveats surrounding exactly what a ‘valid’ application entails.

However this issue continues to trouble various people in the industry, and it is worth clarifying again. Legislative changes for 1.2 ROC qualification are based on the assumption that valid applications were submitted by the end of 22 July 2016. This does not mean that the projects had to be validated by the local planning authority on that day – simply that the paperwork submitted by the developers on that day included the necessary documents that made up a valid project submission.

This is the key differentiator between the words ‘valid’ and ‘validated’. Unfortunately, there is no magic file from the planning resources (local or REPD consolidated) that sheds light on the valid-vs-validated issue, with often only the ‘submission’ or ‘receipt’ date by the LPA being logged. That in itself is often a red herring alone, before we even begin to debate which projects are valid.

Note also there are other conditions for 1.2 ROC validity, including grid-connection offers and evidence of financial commitment by the developers, but it is the ‘valid’ issue that has spooked many not fully in control of the applications submitted on 22 July last year. Anyone in the market today buying consented 1.2 ROC sites is certainly having to bear the upfront legal costs for stringent due-diligence on ROC grandfathering status.

But the fact that deployment has started for 1.2ROCs is extremely positive, and hints at upside to deployment levels under the remaining RO period. Indeed, last week, one of the leading module suppliers and primary site buyers in the UK – Renesola – flagged having almost 300MW of UK solar pipeline with about 50MW in ‘late-stage’. Whether these numbers are real or not (the 300MW seems very high), it does provide a gauge for 1.2 ROC site activity until April 2017.

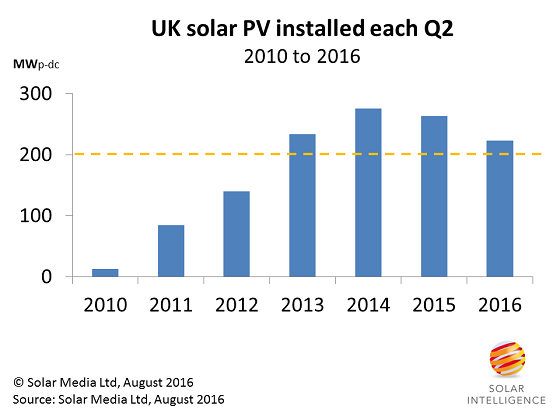

Returning to the Q2 figure of 223MW, and what we can make of this. It should be remembered that the second quarter in the UK has been seasonally weak in the past few years, mainly due to the pull-in for large-scale sites before 31 March each year. The figure below shows second quarter installation data for the UK going back to 2010.

The strong deployment years for solar PV in the UK, under ROCs from 2013 to 2016, have seen second quarter installations trend in the 200-250MW region.

The above graphic is particularly interesting, and does not yet highlight the changes imposed by the government in the past 12 months. However, the figures for Q2 this time around do have a strong contribution from pre-accredited sites – something that is now winding down and will not contribute again in this way.

As we move through H2 2016 and Q1 2017, there will undoubtedly be more striking differences compared to previous quarters, but for now the focus is simply on completing as many 1.2 ROC sites before 31 March 2017, while getting a handle on what Northern Ireland has to offer until 31 March 2018 before the expected start of the Republic of Ireland build phase for solar farms.