The average cost of a 3kW domestic solar installation was nearly £1,000 more expensive in March than it was in January, according to statistics released by the Department of Energy and Climate Change.

Last week DECC released data relating to the average cost of installed solar up to 50kW in size, charting its cost in three separate bands between April 2015 and March 2016.

The data shows that while costs across all three bands steadily declined over the course of 2015, they sharply increased after January, with costs under the domestic band continuing to increase into March.

Costs for 0-4kW installs are now around the £1,900 per kilowatt mark, drastically more than the £1,587/kW average recorded in January. This would mean that the average domestic install of 3kW in size would have been around £1,000 more expensive in March than it was at the start of the year.

Such an increase would stand to have a significant impact not just on the solar industry, but on the validity of the feed-in tariff at its current rate.

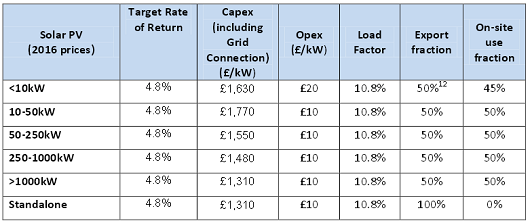

One of the key assumptions in Parsons Brinkerhoff’s report of the feed-in tariff, used to design the new regime, which saw domestic rates fall to as low as 4.39p/kWh, was the average CapEx of £1,630/kW for solar PV under the 0-10kW band.

The new rates have been designed specifically to achieve a targeted return on investment of 4.8%. Such a sharp increase in costs of installation would therefore fail to guarantee consumers the return DECC set out to achieve.

When questioned by Solar Power Portal on the data release, a DECC spokeswoman said: “Our priority is to keep energy bills as low as possible for families and businesses whilst supporting low carbon technologies that represent value for money.

“The cost of solar has steadily declined over the last ten years and it is right that as this comes down so should the consumer-funded support,” the spokeswoman said.

DECC would however not be drawn on the potential implications of surging install costs on available returns.

Leonie Greene, head of external affairs at the Solar Trade Association, warned that the market was “clearly in difficulty” and stressed that low volumes, as seen in the domestic solar industry so far this year, do not lend themselves to low costs.

“We know from our current survey work that some companies are struggling to survive, so every sale matters. The profits on a single install are often pretty modest, so companies need volume for low project returns to make sense.

“It is too early to draw conclusions, but we have always warned that low cost solar depends on a volume market. Maintaining cost reductions requires investment, and that was why we set out a steady glide path to parity for solar in our Solar Independence Plan that would give companies the forward vision necessary,” she added.

While DECC’s FIT review was designed as a cost control measure to tackle an overspend under the Levy Control Framework, the rates and deployment caps have been designed to spend precisely the finance allocated to it. Deployment under the new regime has so far been far below expectations and should it continue to falter, it will raise yet more questions over the much-vaunted LCF overspend.

LCF spending is already in doubt after a third of the five solar projects handed a Contracts for Difference had its subsidy withdrawn in March, with a further project also facing severe delays. The £2 billion Neart na Gaoithe wind farm also had its CfD withdrawn last month.

Former energy secretary Sir Ed Davey has long argued that one of the principal faults in the LCF is the assumption that all projects handed subsidy contracts will go ahead. Any cancelled projects would therefore create an under spend.

The cancellation of wind and solar CfD projects, coupled with flagging deployment under the new FiT regime, would therefore create room under the LCF spending cap for a potential increase in feed-in tariffs needed to stimulate deployment. DECC also has the policy to do so under the FiT review which included a budget reconciliation clause, pledging to biannual reviews of the tariff and expenditure.

DECC continues to monitor the number of installations made under the new regime, but an intervention would be considered unlikely given the department’s desire to allow the tariffs time to bed in.

Last week energy minister Andrea Leadsom responded to a written question by Labour MP Helen Hayes, who sought to acknowledge on what basis solar PV deployment was strong under the new rates.

Leadsom’s reply – that the government remained confident deployment projections would be hit “once transitional and seasonal factors are considered” – would indicate that the government is prepared to at least allow for the summer period, during which time installations have traditionally picked up, to conclude before intervening.

Robert Ede, energy and environment specialist at consultancy group The Whitehouse Consultancy, said it remained unlikely that the government would change the feed-in tariff with other policies currently drawing its attention, but stressed that action was required all the same.

“Recently, Andrea Leadsom stood up in parliament and stated that the government expect rooftop deployment to increase as the industry acclimatises to the new tariffs. However the recent installation data suggests this is a remote prospect. Will DECC be persuaded to take a fresh look at the FiT? Despite recent developments on CfD contracts, this seems unlikely.

“A more profitable route for the industry could be to work alongside the government in opposing the minimum import price (MIP), currently under review by the European Commission. Whilst much of this will depend on the referendum outcome, the removal of the MIP would bring substantial cost savings for installers – and give a significant boost to the UK residential market if we decide to stay within the EU,” Ede said.