The latest monthly release of the UK Battery Storage Project report reveals over 1.3GW of battery storage projects at the ‘ready-to-build’ stage.

Normally, these projects would be expected to get built out over the coming 12 months, and a large proportion would have been completed during 2020. However, it now seems likely that many of these projects will be delayed and could fall into 2021

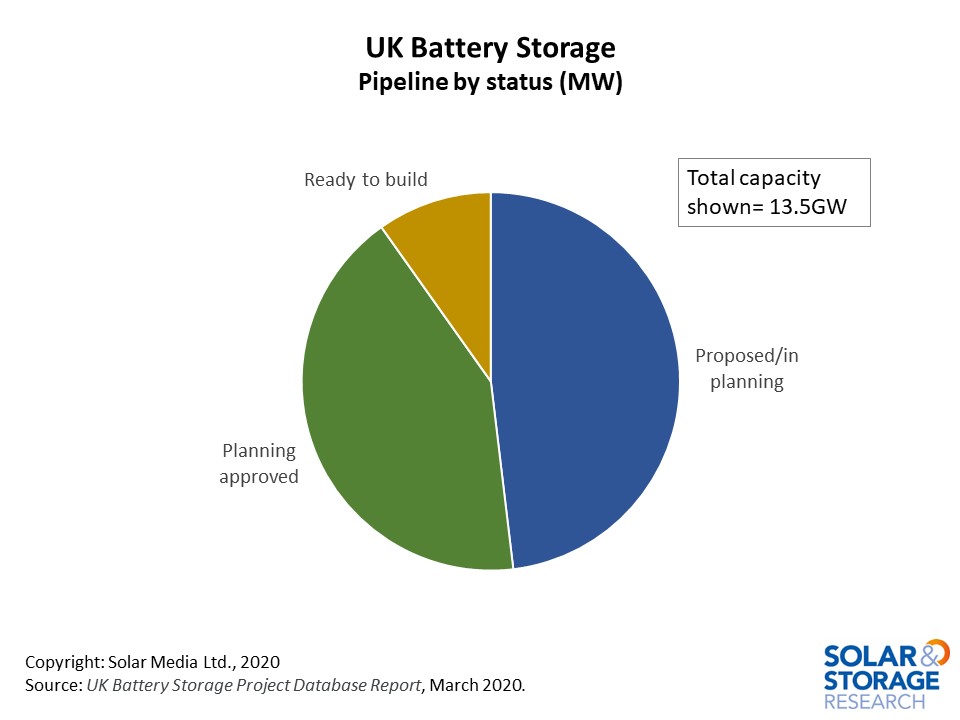

The total pipeline of battery storage projects in the UK has now reached over 13.5GW. The projects identified as being ready-to-build have received planning permission and have other leading indicators suggesting these projects are close to starting construction.

The figure below shows the total pipeline of projects in the UK, minus the 1GW of operational projects.

Activity can be seen across all three categories shown above, while new planning applications continue to be submitted and processed.

We are also seeing activity in the ‘planning-approved’ stage as developers look to progress their pipelines. The activity in this sector will determine pipelines over the longer term; developers and components suppliers will be watching this grouping closely in terms of future opportunities.

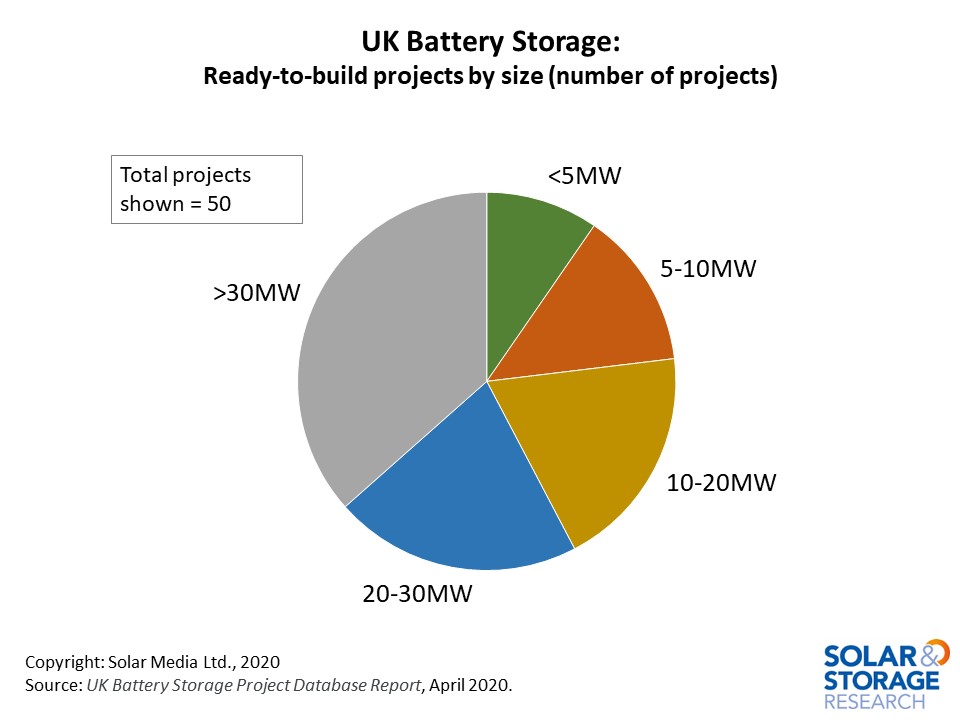

The 1.3GW of ready-to-build projects is analysed in the figure below; the graphic here shows the size of the projects planned.

These projects have secured planning permission, and there are clear indications that this group of projects is progressing. Typically, progress can include site investment, or a contractor/supplier being assigned to the build process.

We can see that a third of the ready to build projects are larger than 30MW and are mostly at the 49.9MW level. The size of these projects means that the capacity built in 2020 will be determined by how many of the >30MW projects are able to be built.

Current uncertainty in the UK arising from COVID-19 naturally means that it is not clear what impact there will be on deployment in 2020; it is too early to redo the forecast for 2020.

However, activity in the first quarter of the year – both from a planning and a corporate perspective – shows that companies are still actively building portfolios of projects and preparing for the build phase. Battery suppliers and other component suppliers are continuing to develop their pipelines and will be looking at strategies to access the large portfolios of projects that are being acquired now. There are also projects in the ready-to-build stage of the pipeline that have Capacity Market contracts due to begin this year, both from the 2016 T-4 auction and the T-1 auction that took place earlier this year.

These projects are already at advanced stages and will be looking to find ways to finish construction. The recent consultation from BEIS to temporarily modify the application of the Electricity Capacity Regulations 2014 and CM Rules will provide some clarity about the requirements and will help lift some of the operational and administrative burdens that would have prevented them from meeting CM obligations.

In the next 12 months, it is not yet clear what precise level of deployment we will see in the UK; but we will continue to see activity in the market and companies will be using the time to finalise plans and strategies for future projects.

The UK Battery Storage Project e report is now being updated monthly by the Solar Media in-house research team to keep up with the rapidly changing market. More information on how to access the report is available here.