Image: Andreas Gücklhorn (Unsplash).

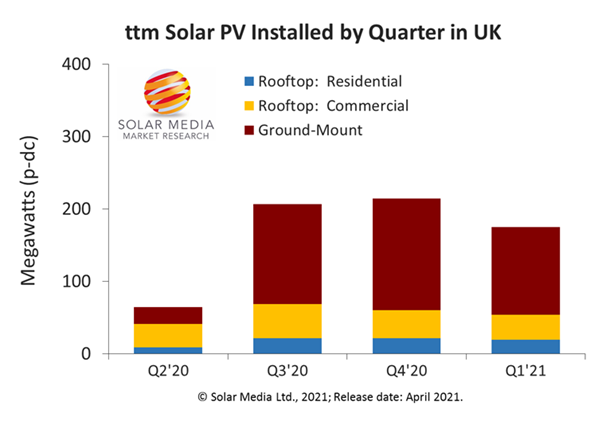

The UK solar industry continued its sustained growth in a zero-subsidy environment, posting 175MWp-dc of new capacity in the 3 months to 31 March 2021 (Q1’21). This was again dominated by ground-mounted solar farms, contributing 70% of the quarterly capacity deployed.

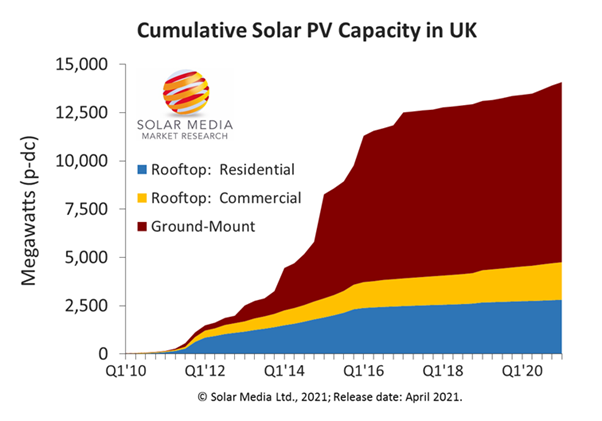

More importantly, since incentives were removed by the UK government (back in Q1’19), more than 1GWp-dc of subsidy-free solar PV capacity has now been installed, marking a landmark moment for the sector as a whole.

The cumulative solar PV capacity installed in the UK is now above 14GWp-dc, of which the subsidy-free part makes up about 7.5%.

The rooftop segments are now operating in a strong-growth and sustained mode, with residential and commercial rooftop installations up 14% year-on-year.

In the twelve months to 31 March 2021, the UK installed 660MWp-dc of new solar PV, setting the calendar year 2021 up nicely for the GW-level, entirely coming in in the absence of subsidies. This would potentially mark the year as the most significant yet for the sector.

The graph below shows the trailing-twelve months to 31 March 2021, by quarter.

The UK solar industry installed 660MWp-dc of new capacity in the twelve months to 31 March 2021, with large-scale solar farms being the key factor in this new post-subsidy growth phase.

The cumulative stack at the end of March 2021 is shown below, confirming the total installed capacity now exceeding 14GWp-dc.

The total installed capacity of solar PV in the UK now exceeds 14GWp-dc at the end of March 2021.

Ground-mount dominates forecasts but phasing of builds uncertain

The major growth is coming of course from large-scale solar farms. In this respect, the UK is no different from other countries and regions globally. The PV industry this year is likely to see more than 190GW of new capacity added, more than 80% of this coming from ground-mounted solar farms. Rooftop segments are now – by comparison – a small part of a very large industry.

In the past 12 months, six solar farms each with capacity above 40MWp-dc have been completed, with the largest (75MWp-dc) finished during Q4’20 but announced ‘officially’ by its owners a few weeks ago. This trend of announcing sites after-the-event is becoming the new norm in UK solar; indeed, two of these large-scale solar farms have been absent of any marketing bling from owners/builders/suppliers as if stealth operations were the order of the day.

Large-scale solar farms will continue to dominate UK solar for the next decade, at the 80%-plus capacity level. Fuelling this is a rapidly-growing pipeline of new site projects added every month. During the past year, more than 800MW per month average has been added by way of new sites, with most of these at pre-application stages.

The outlook for 2021 remains at the GW-level of new solar PV capacity added in the UK. The determining factor however is completely out the hands of anyone in the UK, but is purely a function of raw material supply availability to serve the global sector during the year.

Let’s talk about this more, as it is the single most important issue impacting the global sector today.

More than 95% of solar panels are comprised of solar cells made from wafers (the bulk material). These wafers are sliced from ingots pulled from chunks of polysilicon. Across the value-chain, there is ample capacity of ingot pullers, wafer slicing machines and cell/module production fabs. The problem right now lies purely at how much polysilicon can be supplied to the ingot pulling fabs in China. About 99% of ingots are pulled in factories in China today.

During 2019 and 2020, about half a dozen loss-making polysilicon producers exited the industry. Then in the middle of 2020, there were several explosions and natural disasters in China that took a bulk of the Chinese polysilicon capacity offline. This led to a shortage of polysilicon. In turn, the polysilicon suppliers put prices up. This tightness in supply has not changed today. Polysilicon now costs about twice that of 12 months ago.

In addition, during the second half of 2020, there was a shortfall of glass in China. The polysilicon tightness, coupled with the glass supply downturn, had the dual effect of adding 15-20% to module prices. This situation has persisted since the start of the year, although one of the contributing factors (glass) has now eased off. Lack of polysilicon however continues to be a problem.

This module price increase (globally) effectively means that project margins (especially in post-subsidy days) get compressed, and potentially below the go-ahead threshold. Since zero-subsidy means no deadlines to build, the net impact is projects get pushed out, in the hope that module pricing returns to the mid-2020 levels, before the increases brought about by polysilicon and glass supply tightness.

The UK is not lacking approved large-scale solar farms, many of which are currently going through final conditional approval condition sign-off. However, build-out would ideally be when module pricing is lower than the highs of the past 3-4 months.

Forecasting when the module pricing will return to Q3’20 levels is not trivial, but thankfully not as hard as forecasting winning lottery numbers.

Within China, there are 3-4 large polysilicon plants that are in construction. The prevailing wisdom a few months ago was that they would add to supply capacity at the start of 2022. However, there is a massive drive (not unexpectedly) to bring forward production dates well into 2021. If this happens, then module pricing may well start to ease downwards in Q3’21, and then keep falling in the final quarter. If these new sites remain 2022 plays, then current module pricing could stay firm all this year. It is a tough one to call right now.

Ultimately, this may be the one factor that determines if the UK installs south of 1GW during 2021 (possibly in the 850-900MW range) or exceeds 1GW (as high as 1.5GW) if a second half and year-end blitz of new building unfolds.

Understanding more about the UK solar market in 2021 and beyond

Solar Media continues to be the go-to resource for all stats on UK solar deployment and forecasting. To access our databases of sites (both completed and forecast), more details can be found at our market research link here.

Additionally, we are holding the first ever dedicated conference for large-scale solar farms in the UK on 15-16 June 2021, the Utility Scale Summit UK. To be held online, this two-day event will focus on all the key themes necessary for site stakeholders (investors, component suppliers, EPCs, etc.) to maximise sales prospects this year and beyond. To get involved in the Utility Scale Summit UK event, please register interest here.