According to the latest release of Solar Media’s UK Ground-Mount Report 3 – Opportunity Pipeline report, the UK’s pipeline of large-scale solar farms (>250kW) has grown now to 3.3GW. This is due mainly to an increase in applications received by LPAs on 22 July, and an uptick in rejected (or called-in) sites to appeals.

Counting all the sites across large-scale FiTs (>250kW) and potential 2014 and 2015 grace-complaint 1.3RO qualification, there are now almost 600 projects making up the 3.3GW figure. This figure is expected to plateau in the next month, as final validation is acknowledged across the 400 different LPAs in the UK and some of the more recent sub-5MW rejections are added to the appeals queue.

The sixty-four-thousand-dollar (or should that be Greg Barker’s 2012 coined phrase – the Big 60 Thousand) question for DECC is what is going to happen under the remaining, albeit likely curtailed, lifetime of solar based ROs.

Interestingly, the pipeline of 600 solar farms adding to 3.3GW all had planning applications submitted before midnight on 22 July 2015. And we have excluded CfD sites and everything NIROC from the above analysis, so what we have is the most accurate pipeline analysis on the go right now.

So – let’s dissect the data bottom-up and get an idea where it is coming from. This is shown in the figure below.

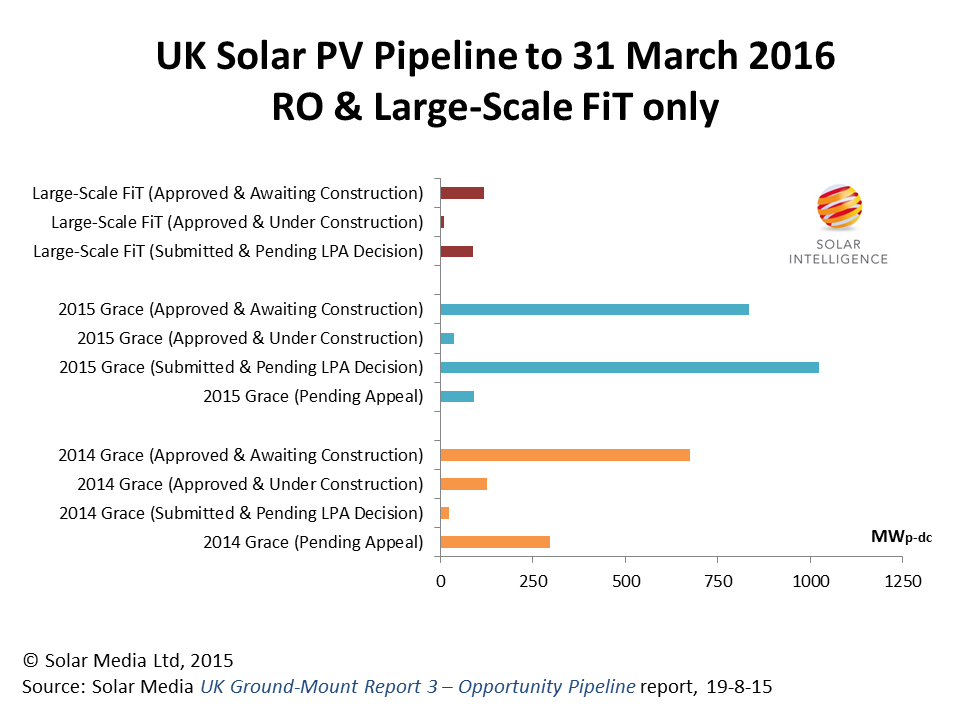

Figure Caption: The pipeline of approximately 600 solar farms, adding to 3.3GW, can be split into eleven different categories, depending on RO ‘grace-year’ and status of the submitted application. Source: Solar Media UK Ground-Mount Report 3 – Opportunity Pipeline report, 19 August 2015.

The legacy hangover from DECC’s 2014 RO changes is still clear to see, even before DECC finalises its 2015 grace conditions. And added to the mix are sites at appeal, a bunch which are highly unlikely even to come out of the appeals process before 31 March 2016. Unless that is, DECC decides to grant the solar industry similar fast-tracking legislation changes it is proposing for shale-gas. But if you think that is likely, you are dreaming.

What the pipeline figure of 3.3GW by 31 March 2016 really means is the absolute maximum. In marketing terms, we can call this the total addressable market, or TAM. No-one ever hits 100% of TAM in business, and it is the served addressable market (or SAM) that is more indicative of the real world.

So, what is the UK’s ground-mounted SAM for large-scale deployment to 31 March 2016? Well, to get this, you need to know the details on the 600 sites and access how many are going to happen, through some different scenarios. What the government would do in an Impact Assessment, for example, but of course coming from a top-down approach, not a site-specific bottom-up approach.

Is the SAM going to be 10% of the TAM, given all the risks? So, about 330MW deployed to 31 March 2016? Or higher?

Because there is an ongoing consultation between DECC and the industry regarding RO changes, and discussions that demand in particular that DECC has its own forecasts (to base its RO estimates on), we are not going to publish our RO forecasts until DECC issues its final ruling. Then we will start to dissect and analyse all the sites that make up the eleven different categories shown in the attached figure.

Details on the 600 sites, including CfD and NIROC candidates, are available in this week’s release of our UK Ground-Mount Report 3 – Opportunities Pipeline report, with information on this available here.